Written By: Aanchal Saini

Let me tell you a small story.

A shop owner in Kanpur is looking for industrial glue for making furniture. At the same time, a factory in Vapi has that glue, packed and ready in bulk. The two don’t know each other. But somehow, they connect and do business.

Not through Amazon. Not through a phone call. But through a website called IndiaMART.

IndiaMART isn’t like Flipkart or Zomato. You don’t shop for clothes or order food here. This is a website where businesses buy and sell to other businesses — also called B2B (business-to-business). And this happens millions of times across India, every month.

Most regular people may not use IndiaMART. But behind the scenes, it’s a big player in India’s digital business world.

Now, something happened in late 2024 that made people worry — IndiaMART lost some of its paying customers. But what’s interesting is how the company fixed it — quietly, smartly, and without making a big show.

Let’s break it down.

What Went Wrong?

At the end of 2024, things looked good. IndiaMART had:

- Over 84 lakh suppliers listed on the platform

- More than 21 crore buyers

- Strong profits, better than many tech companies

But then, something changed.

In the third quarter of FY25, about 4,000 paying subscribers left the platform. That’s around 2% of the base. It may seem small, but it raised a red flag.

Why? Because most of the people who left were Silver plan users — the basic, entry-level paying customers. These are often small business owners who are just starting to use digital platforms. If they leave early, they don’t get a chance to upgrade to higher plans — and that hurts the long-term growth.

So the drop wasn’t just about numbers. It was about the quality of users who were leaving.

Investors began to ask:

- Are the leads no longer useful?

- Are small sellers losing interest?

- Is a competitor offering something better?

One big brokerage house, Nuvama , even downgraded the stock. The share price started falling. But instead of panicking, IndiaMART took a step back — and got to work.

How Did IndiaMART Fix It?

Here’s what IndiaMART didn’t do:

It didn’t start giving discounts.

It didn’t spend crores on ads.

It didn’t try to grow just for show.

Instead, it focused on what was broken — and fixed it.

- First, it brought its sales team in-house. Earlier, another company handled sales. Now, IndiaMART took full control. This helped them make sure leads were better matched and results were tracked properly.

- It improved its lead engine — the system that connects buyers to sellers. The goal was to make sure suppliers get leads that actually matter to them.

- For Silver users, IndiaMART gave more support. This included better onboarding, help with setting up profiles, and faster customer service.

- Sales targets were changed. Earlier, salespeople were rewarded for getting new sign-ups. Now, they were rewarded for getting good customers who stay longer.

These changes were not big news. But they worked. In just one quarter, things improved. Fewer people were leaving, and new user growth started again.

Let’s Look at the Numbers

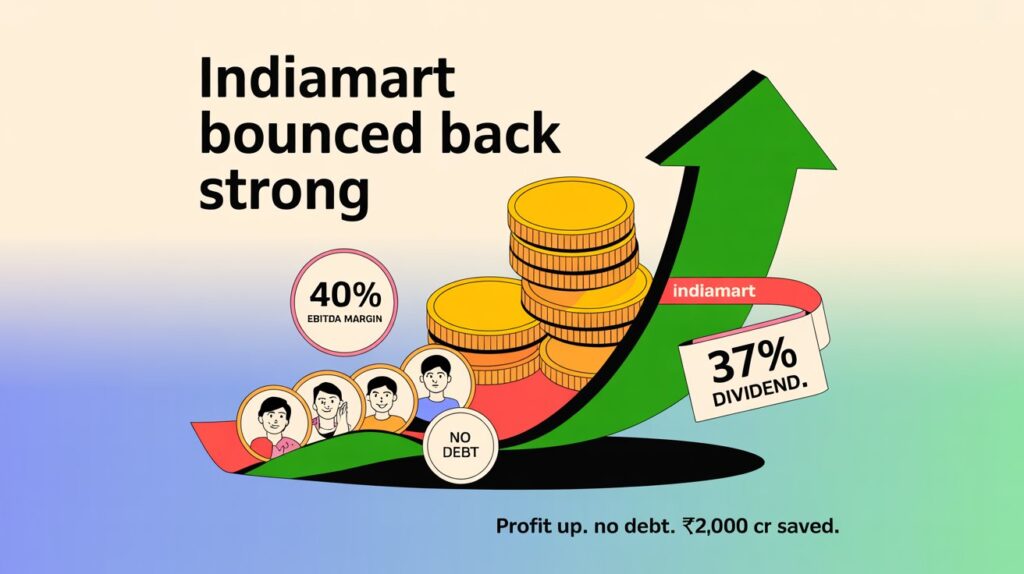

By the end of FY25, IndiaMART shared its latest performance — and it was strong:

- Revenue grew 16% to ₹1,388 crore

- EBITDA margin was close to 40% — this means IndiaMART is very profitable

- 58% of buyers came back to make repeat purchases

- IndiaMART allows users to pay monthly, yearly, or even for multiple years. So the company collects money in advance — shown as something called deferred revenue. About 20% of this revenue gets counted within 3 months, which helps cash flow.

- The company has over ₹2,000 crore in reserves (money saved)

- And it has almost no debt

- It even gives regular dividends — around 37.3% payout

These numbers show that IndiaMART is well-managed, cash-rich, and trusted by its users.

What Should You Watch Next?

IndiaMART’s story is not just about fixing one problem. It tells us something deeper:

- It doesn’t run after quick growth. It builds slow, steady, and meaningful growth.

- Its subscription model brings in stable income.

- The more buyers and sellers join, the stronger the platform becomes — this is called a network effect.

- IndiaMART has survived many tough periods — the dot-com crash, the 2008 crisis, even COVID. It never needed big loans or rescue packages. It just adapted and kept going.

That kind of history builds trust — both for users and for investors.

What’s the Future Plan?

India’s small businesses — also called MSMEs — are going online fast. From GST to payments to payroll, everything is going digital. And IndiaMART wants to help with that journey.

So, it’s now offering extra tools like:

- Accounting software

- Delivery and logistics tech

- Payroll services

These are still small parts of revenue (only about 5%), but they could grow in the future. The idea is to go beyond just giving leads — and become a complete business partner.

Imagine a small manufacturer who not only finds buyers on IndiaMART but also tracks his orders, manages accounts, and pays his staff — all from one platform.

That’s the goal.

Final Thought

And now, with subscriber growth back, brokerages are returning too — Nuvama raised its valuation multiple from 22x to 35x.

IndiaMART could have reacted with noise, ads, and offers.

Instead, it quietly fixed its own system.

In today’s world, where companies shout at every little update, IndiaMART’s calm and thoughtful approach stands out.

It shows that real strength lies in knowing what to fix — and doing it right.

The company isn’t just surviving. It’s slowly becoming a core part of India’s business world. And if it keeps moving with the needs of small businesses, it won’t just bounce back from a bad quarter — it will become stronger and more useful over time.

For investors and anyone watching India’s digital economy — this is a company worth keeping an eye on.

Not just for a quick profit.

But for the long run.