Written By: Soumya Singhal

Companies capitalize rather than expense a purchase when the item provides future economic benefits beyond the current accounting period. Capitalizing spreads the cost over the asset's useful life, aligning expenses with the revenues they help generate, a practice based on the matching principle in accounting.

The difference between capitalization and expense lies in how a company records a cost on its financial statements and how it affects profitability over time. Here’s a breakdown:

| Aspect | Capitalization | Expense |

| Definition | Recording a cost as an asset on the balance sheet to be depreciated or amortized over its useful life. | Recording a cost directly on the income statement reduces profits in the current period. |

| Purpose | Used for expenditures that provide long-term benefits. | Used for expenditures that provide short-term benefits. |

| Accounting Treatment | Added to the balance sheet as an asset and depreciated/amortized over time. | Recorded as an expense on the income statement in the period incurred. |

| Effect on Net Income | Spreads the cost over several periods, minimizing the immediate impact on net income. | Reduces net income in the period it is incurred. |

| Impact on Financial Statements | Increases in assets on the balance sheet and delays impact the income statement. | Reduces net income and retained earnings immediately. |

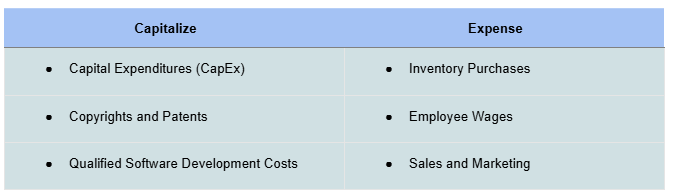

| Examples | - Purchasing machinery, buildings, or software.- Construction of a new factory.- Development of a patent. | - Office supplies.- Salaries and wages.- Utility bills.- Routine maintenance. |

| Impact on Cash Flow | Recorded in the investing activities section of the cash flow statement. | Recorded in the operating activities section of the cash flow statement. |

| Financial Ratios | Improves profitability ratios (e.g., EBITDA, net profit) in the short term. | Immediately reduces profitability ratios. |

| Depreciation/Amortization | Depreciated (for tangible assets) or amortized (for intangible assets) over time. | No depreciation or amortization; fully expensed in the current period. |

Generally, one useful question is, “Will the cost continue to provide benefits for more than a year?”

- Yes?✅ → Capitalize

- No?❌ → Expense

If the anticipated useful life exceeds one year, the item should be capitalized – otherwise, it should be recorded as an expense.

- Capitalizing → The expenditure is recognized on the balance sheet as an asset, and then the asset is reduced by depreciation or amortization annually, which is an expense on the income statement.

- Expensing → The cost is recognized as an expense on the income statement in the same period as when the expense was incurred.

The primary objective of capitalizing a cost is to align the timing of the expense with the economic benefits it generates, by the Matching Principle. (The Matching Principle states the expenses of a company must be recognized in the same period as when the corresponding revenue was “earned.”)

Based on the asset's estimated useful life, the cost is gradually expensed over time until the asset no longer provides economic value to the company.

Expense Recognition:

- Fixed Asset (PP&E) → Allocated through Depreciation Expense

- Intangible Asset → Allocated through Amortization Expense

In contrast, if an expenditure and its associated benefit are expected to be fully utilized within a year, the cost should be expensed in the period it is incurred.

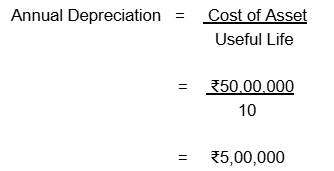

Example: Depreciation of Machinery

A company purchases manufacturing equipment for ₹50,00,000 on January 1, 2024. The equipment has an estimated useful life of 10 years with no salvage value.

Accounting Treatment:

- The company capitalizes the ₹50,00,000 as a fixed asset on the balance sheet.

- The cost is expensed over time through depreciation.

Using the straight-line depreciation method, the annual depreciation expense is:

Journal Entries:

At the time of purchase (January 1, 2024):

At the end of each year (e.g., December 31, 2024):

Financial Impact:

- Year 1 (2024):

- Depreciation Expense of ₹5,00,000 is recorded in the income statement, reducing the company's net profit.

- The remaining net book value of the asset on the balance sheet is ₹45,00,000 (₹50,00,000 - ₹5,00,000).

- Year 10 (2033):

- After 10 years, the asset is fully depreciated, and its net book value becomes ₹0.

- The total ₹50,00,000 has been expensed over its useful life, reflecting that the asset no longer contributes to the company’s economic output.

Example: Inventory As Expense Recognition

Inventory purchases are typically cycled out quickly unless the company faces inefficiencies in managing working capital. As a result, inventory is classified as a short-term asset, expected to be sold or used within one year.

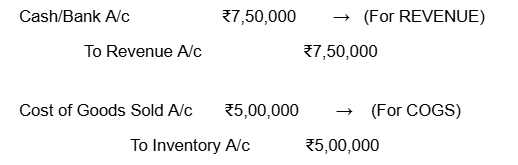

A company purchases raw materials for ₹5,00,000 on January 1, 2024, intending to use them in production. The finished goods are sold by March 31, 2024, for ₹7,50,000.

Journal Entries:

At the time of purchase (January 1, 2024):

When the inventory is used in production (e.g., February 15, 2024):

When the finished goods are sold (March 31, 2024):

Financial Impact:

- Inventory (₹5,00,000) is initially recorded as a current asset.

- Once sold, the ₹5,00,000 is expensed as COGS, reducing the gross profit for the period.

- The company earns a gross profit of ₹2,50,000 (Revenue ₹7,50,000 – COGS ₹5,00,000), reflecting the short-term economic benefit of the inventory.

Capitalize or Expense: Common Real-Life Examples

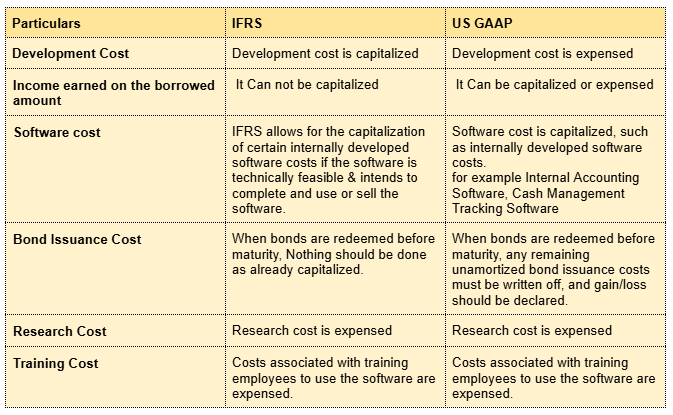

Capital & Expense has different rules in US GAAP and IFRS

US GAAP and IFRS are the two leading accounting standards used by public companies worldwide, each with distinct financial reporting guidelines.

Publicly traded companies must prepare their financial statements according to specific accounting standards to provide a fair and accurate representation of their operations.

US GAAP:

In the United States, public companies follow the Generally Accepted Accounting Principles (US GAAP), established and regulated by the Financial Accounting Standards Board (FASB).

IFRS:

In contrast, more than 144 countries adhere to the International Financisal Reporting Standards (IFRS), developed and maintained by the International Accounting Standards Board (IASB).

There are four main areas where the two diverge in financial reporting:

- Financial Statement Presentation

- Recognition of Accounting Elements

- Measurement of Accounting Elements

- Disclosures and Terminology

Difference of Recognition of Accounting Elements between IFRS and US GAAP